- SAP Community

- Groups

- Interest Groups

- Sustainability

- Blogs

- SAP Sustainability for Financial Services – Regul...

Sustainability Blogs

Delve into SAP sustainability blogs. Gain insights into tech-driven sustainable practices and contribute to a greener future for businesses and the planet.

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Associate

Options

- Subscribe to RSS Feed

- Mark as New

- Mark as Read

- Bookmark

- Subscribe

- Printer Friendly Page

- Report Inappropriate Content

12-20-2023

10:37 AM

First of all, I would like to introduce myself. My name is Denise Iwersen and I am a Customer Advisor for Financial Services at SAP Germany. In my recent blog post, I focused on the EU Taxonomy its importance to the financial industry and the SAP portfolio that can be used to implement the EU Taxonomy.

This blog post is intended to become part of a series of blog posts to deepen the topic of sustainability in the financial industry. This blog post first examines and explains the regulatory requirements for the financial industry in more detail. The following blog posts are intended to provide an insight into the SAP Sustainability Portfolio and explain how SAP can help its customers in the financial industry with their products.

As described in the previous blog post, the topic of sustainability is not just a trend, but is often part of the company’s culture. For example, according to the EU Taxonomy, companies have already been required to publish first sustainability metrics since 1st January 2022.[1] In particular, banks and insurers face major challenges in implementing regulatory requirements. Firstly, financial services providers must implement the requirements of the EU Taxonomy. This includes the calculation of the key figures ‘Green Asset Ratio (GAR)’ and ‘Banking Book Taxonomy Ratio (BTAR)’. The former key figure must be reported in January 2024 for the financial year 2023 (see previous blog post).

In addition to the EU Taxonomy, the ‘Corporate Sustainability Reporting Directive’ (CSRD) is of great importance in the context of ESG reporting in the EU. The CSRD is a standard set by the ‘European Financial Reporting Advisory Group’ (EFRAG) and defines, as part of the EU Taxonomy, principles for companies to disclose sustainability information as part of the annual financial statements. It replaces the so-called ‘Non-Financial Reporting Directive’ (NFDR), whereby the number of users will significantly increase. According to estimates, the number of reportable companies is thus increasing from 11,600 to 49,000 across the EU.[2] The CSRD officially entered into force in January 2023 and is effective from 1st January 2024 for large companies with more than 500 employees. Other companies will be required to report in the following years. Although the directive has not yet been transposed into German law, the member states of the EU have 18 months to transpose it into national law after the CSRD has entered into force. The CSRD, on the one hand, is refering to the EU Taxonomy by requesting the reporting requirements under Article 8 of the EU Taxonomy.[3] On the other hand, the CSRD refers to the ‘Greenhouse Gas Protocol’ (GHG) and its concept of scopes. In this regard, Article 47 of the CSRD requires that information relating to Scope 3 emissions must be included in the sustainability reporting. This article also makes clear that although the CSRD describes the disclosure requirements, no requirements are made with regard to which kind of information are to be disclosed. With reference to Article 29b of the CSRD, the European Commission must therefore establish further standards for sustainability reporting. [4] On the 22nd November 2022, the first draft of the ‘European Sustainability Reporting Standards’ (ESRS) was therefore published by EFRAG as a technical consultant to the Commission.[5] In particular, ESRS should take into account and reflect international regulations. The relationship between the ESRS and the EU Taxonomy, as well as the SFDR and other regulations, are described in the Explanatory Note [6]. Equally to the CSRD, the ESRS must also be implemented by January 2024. First reports under CSRD are to be published as of 2025.[7]

The ESRS are sector-agnostic and consist of 12 so-called ‘Exposure Drafts’ (ED), which in turn are divided into two cross-sector EDs (ESRS1 + ESRS2), as well as ten topic-specific EDs. In total, ESRS include 82 ‘Disclosure Requirements’ (DR), divided into the twelve different EDs.

Figure 1: Overview of DRs per ED [8]

All companies falling within the scope of ESRS must comply with and implement the requirements of the two sector-agnostic EDs ESRS 1 and ESRS 2. [9] In order to analyse which requirements of the topic-specific EDs from the ESRS E1-5, S1-4 and G1 are to be implemented, companies must carry out a “materiality analysis”. The materiality analysis shall be carried out for all topic-specific ESRS. Once an issue has been defined as material in accordance with ESRS 1, Section 3.4 and 3.5, it must be disclosed in accordance with the disclosure requirements of the respective standard.[10] The result of this analysis determines which disclosure requirements are to be presented in a report.

As required by the CSRD, ESRS follows the principle of ‘double materiality’. This means that companies, regardless of industry, need to do sustainability reporting from two perspectives:

Although all disclosure requirements are to be integrated into the annual report in accordance with the respective materiality analysis in the future, ESRS offers a transitional period to implement the requirements. Annex D of ESRS 1 lists the requirements (DRs) that may first be omitted or that must be implemented at a later point in time. [13]

In the previous section, the current requirements of CSRD and ESRS have now been outlined. No distinction has been made for different industries up to now. But what does this mean for financial institutions that differ significantly from other industries in their business models?

As mentioned above, the CSRD, and therefore the ESRS, refers to the concept of the ‘Greenhouse Gas Protocol’ (GHG), whereby emissions must also be disclosed in Scope 1, 2, and 3. In particular, Scope 3 emissions are of central importance for banks and insurers because most of the emissions caused are not from their own sources, but from financial instruments or insurance activities. This corresponds to the definition of Scope 3 emissions, which include all indirect emissions from sources that are not owned or controlled by the company. Scope 3 Emissions correspond to emissions that occur in the company's value chain.[14] It is estimated that Scope 3 emissions for banks and insurers are 700 times larger than direct Scope 1 and Scope 2 emissions.[15]

The EFRAG Draft ‘Implementation Guidance for Value Chain’ (VCIG) explains the extent to which emissions from the value chain are to be included in the materiality analysis and, consequently, in the calculation and disclosure. For banks and insurers, this means that emissions from investments made, as well as emissions from loans or insurance issued, would have to be calculated and disclosed. However, to implement this, information is required from the borrowers and policyholders, some of which are not publicly available.

For the financial industry, the question here is how to include information from business partners and customers in the calculation and disclosure of sustainability metrics.

In the VCIG, EFRAG does not provide a clear answer to the ‘HOW’. It is noted that “financial assets”, including loans and investments, are interpreted as “business relationships” and therefore fall within the scope of the value chain.[16] For example, if the company grants loans to another company, which is ultimately used to implement a project that in turn leads to water pollution, this influence must also be attributed to the lender.[17]Although it is established that the indirect Scope 3 emissions of financial institutions must also be calculated and disclosed, no standards have been published so far to implement these requirements for financial institutions by EFRAG or other European institutions.[18]

For this reason, the draft ESRS has so far referred to other initiatives. ESRS requires financial institutions to use the requirements of the ‘Greenhouse Gas Accounting and Reporting Standard for Financial Industry’ (PCAF) to disclose Scope 3 emissions.[19] The ‘Partnership for Carbon Accounting Financials (PCAF)’, which develops this standard, is a global partnership of different financial institutions that jointly develops approaches to assess and disclose greenhouse gas emissions related to loans and investments.[20] In principle, accession to the partnership is voluntary, but application of the PCAF standards is mandatory upon accession. [21]

Based on the ‘GHG Corporate Accounting and Reporting Standard’ and the ‘Corporate Value Chain (Scope 3) Accounting and Reporting Standard’, the PCAF Standard provides standardized methods for measuring “financed” and “insured emissions”. This will continue to enable financial institutions to develop new strategies and innovative financial products. The PCAF standards consist of the following three parts:

Part A ‘Financed Emissions’ includes the calculation methods for measuring and disclosing emissions related to different asset classes.

Part B ‘Facilitated Emissions’ provides calculation methods to determine the issues related to capital market transactions.

Part C ‘Insurance Associated Emissions’ includes calculation methods for determining issues related to insurance and reinsurance. [22]

However, for the calculation of Scope 3 emissions, ESRS refers only to ‘financial institutions’. There is no definition of the term ‘financial institution’, including a clear distinction between banks and insurance companies. In addition, ESRS requires screening of Scope 3 emissions based on the 15 Scope 3 categories of the ‘GHG Protocol Corporate Standard’ and the ‘GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard’.[23] However, these 15 Scope 3 categories do not cover insurance business. Therefore, the ESRS is assumed to refer only to Part A of the PCAF standard (‘Financed Emissions’) and emissions related to insurance (‘Insurance Associated Emissions’=IAE) are not taken into account. It is therefore important to clarify how the IAE are to be calculated and disclosed. Associations, including the Association of the German Insurance Industry, demand sector-specific ESRS for insurance, as well as more lead time for implementation.[24] For the given reason, the focus of the following section is therefore only on 'Financed Emissions'.

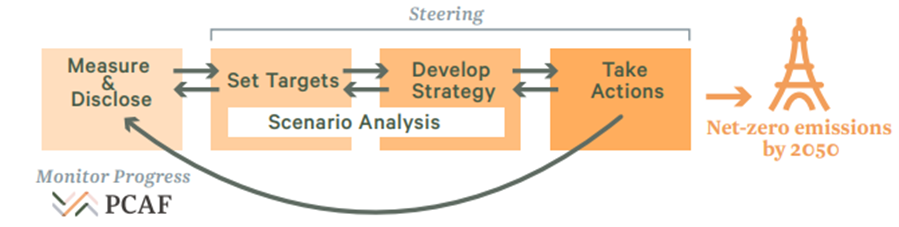

The application of the PCAF standards primarily serves to measure and disclose the greenhouse gas emissions caused by investments and credits. The measurement of these emissions forms the basis for identifying risks and opportunities associated with the formation of greenhouse gases and thus enabling decarbonization. In addition, the results of these calculations serve as a basis for the development of strategies and products to enable the achievement of climate targets.

Figure 2: PCAF as a start to achieve climate objectives [25]

The PCAF standard for ‘Financed Emissions’ (Part A) includes calculation methods for seven different asset classes, whereby separate requirements are described for each class:

A method is also provided by PCAF to determine which asset category is to be applied for each financial product. The determination takes place in three steps and follows the ‘follow-the-money principle’:

Figure 3: Derivation of the applicable asset class and calculation method [27]

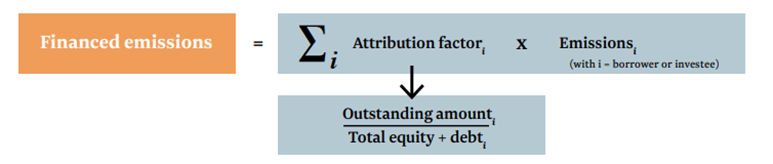

Once the asset class is determined, the emissions can be calculated. The PCAF standard thereby follows the attribution principle. According to the ‘GHG Protocol Value Chain Accounting and Reporting Standard’, GHG issues from loans and investments are to be allocated to the financial institution based on the share of loans and investments in the borrower. In other words, the financial institution is responsible for a share of the emissions of the borrower.

The calculation of the ‘Financed Emissions’ is done for all asset classes equally, based on the annual emissions of the borrower. To do this, an attribution factor is first calculated. This is the share of the remaining amount of a loan or investment (numerator) in the total equity and debt of the company or project to which the financial institution provides capital (denominator). This “attribution factor” must afterwards be multiplied by the total emissions of the borrower. A differentiation of the applicable value in the denominator results from the methods to be used for the asset classes.[28]

The calculation of the ‘Financed Emissions’ requires, as described, information about the emissions of the borrower. This information is either provided by the borrower or can often already be taken from a sustainability report from the borrower. However, the quality of this data can vary between companies with regard to e.g. timeliness and correctness. For this reason, PCAF also provides a scoring model to evaluate the quality of the underlying data.

The scoring model consists of five levels, where data classified with 'Score 1' potentially has the best data quality. ‘Score 5’ represents the potentially worst data quality. Data quality scoring is different for each asset class. Basically, it is advised to use the best possible data but PCAF dictates what kind of information to use in each score for each asset class.[29] These are listed and explained in the appendix to the ‘Financed Emissions’ standard for each asset class. The following image shows the options using project financing as an example. Here you can clearly see the differences in the information to be applied and their accuracy in the individual scores.

Figure 6: Data Quality Score for Project Financing[30]

In summary, PCAF is a good approach to calculating financed and insured emissions. Nevertheless, the standard does not allow a complete and accurate presentation of Scope 3 emissions from financial institutions. Firstly, there seem to be no clear recommendations by ESRS for insurance companies, which means it is up to the companies themselves to determine which calculation method is to be used for Scope 3 emissions. As a result, comparability between insurers in terms of their Scope 3 emissions would be hampered. On the other hand, as described, PCAF also allows the use of different data qualities. While PCAF also provides a scoring model to standardize data qualities, this means that financial institutions may also use incomplete or even unverified information about customers to calculate emissions from financing and investment activities. Although the data quality score must be disclosed in addition to the metric, heterogeneous data quality leads to a difficult internal comparability between parts of the portfolio, as well as externally between companies and projects.

The fact is that financial institutions have to implement the requirements of the CSRD, and therefore the requirements of ESRS, partially as of January 2024. Even though it appears no clear requirements for the calculation and disclosure of Scope 3 emissions have been published for insurance companies, financial institutions are already asked to use the PCAF standard to calculate the Scope 3 emissions from financing and investment activities. However, these are one of the biggest challenges financial institutions are facing. In particular, the availability and validation of customers’ sustainability information is a challenge. In addition, financial institutions need to find technical solutions to store the collected information of business partners and customers in a consolidated manner and, based on this, to calculate and disclose the key figures required by the regulatory frameworks.

SAP’s sustainability portfolio can help financial institutions to overcome these challenges. In a following blog post, the current SAP portfolio for sustainability in the financial industry shall be presented and explained. In particular, the technical implementation of the regulatory requirements of the CSRD and ESRS is planned to be examined in more detail.

References:

[1] EU Taxonomy Regulation (EU) 2020/852

[2] CSR - Corporate Sustainability Reporting Directive (CSRD)

[3] CSRD - DIRECTIVE (EU) 2022/2464 - (46)

[4] CSRD - DIRECTIVE (EU) 2022/2464 – Article 29(b)

[5] EFRAG, November 2022 - ESRS Cover Letter

[6] EFRAG, November 2022 – ESRS Explanatory Note

[7] EFRAG - First Set of Draft ESRS

[8] Cf. ESRS, Appendix I Disclosure Requirement Index – Table 2 ‘Overview of DRAFT ESRS’

[9] ESRS 1 – November 2022, Chapter 3.2

[11] ESRS 1, November 2022, Chapter 3.4

[12] ESRS 1, November 2022, Chapter 3.5

[13] ESRS 1, November 2022, Chapter 10.4 & ESRS 1 – November 2022, Appendix D

[14] Corporate Value Chain (Scope 3) Accounting and Reporting Standard, Chapter 5

[15] S&P Global – Podcast ‘How financial institutions are tackling Scope 3 funded emissions’

[16] EFRAG – Implementation Guidance for Value Chain (VCIG), 23. August 2023, para. 56

[17] ESRS 1 – November 2022, AR 7(b)

[18] EFRAG – Implementation Guidance for Value Chain (VCIG), 23. August 2023, para. 58

[19] ESRS E1, November 2022, Appendix B, AR 44 (b)

[20] PCAF – About PCAF

[21] PCAF - How to Join PCAF

[22] PCAF - The Global GHG Accounting and Reporting Standard for the Financial Industry

[23] ESRS E1, November 2022, Appendix B, AR 44 (c)

[24] GIA – Comment on the first set of draft European Sustainability Reporting Standards

[25] PCAF – Financed Emissions Standard

[26] PCAF - ‘Financed Emissions’ Standard – Chapter 5

[27] PCAF - ‘Financed Emissions’ Standard – Chapter 5, Figure 5-1.

[28] PCAF - ‘Financed Emissions’ Standard – Chapter 4 & Chapter 5

[29] PCAF - ‘Financed Emissions’ Standard – Chapter 4.2

[30] PCAF - ‘Financed Emissions’ Standard, Annex 10.1, Table 10.1-3

This blog post is intended to become part of a series of blog posts to deepen the topic of sustainability in the financial industry. This blog post first examines and explains the regulatory requirements for the financial industry in more detail. The following blog posts are intended to provide an insight into the SAP Sustainability Portfolio and explain how SAP can help its customers in the financial industry with their products.

As described in the previous blog post, the topic of sustainability is not just a trend, but is often part of the company’s culture. For example, according to the EU Taxonomy, companies have already been required to publish first sustainability metrics since 1st January 2022.[1] In particular, banks and insurers face major challenges in implementing regulatory requirements. Firstly, financial services providers must implement the requirements of the EU Taxonomy. This includes the calculation of the key figures ‘Green Asset Ratio (GAR)’ and ‘Banking Book Taxonomy Ratio (BTAR)’. The former key figure must be reported in January 2024 for the financial year 2023 (see previous blog post).

In addition to the EU Taxonomy, the ‘Corporate Sustainability Reporting Directive’ (CSRD) is of great importance in the context of ESG reporting in the EU. The CSRD is a standard set by the ‘European Financial Reporting Advisory Group’ (EFRAG) and defines, as part of the EU Taxonomy, principles for companies to disclose sustainability information as part of the annual financial statements. It replaces the so-called ‘Non-Financial Reporting Directive’ (NFDR), whereby the number of users will significantly increase. According to estimates, the number of reportable companies is thus increasing from 11,600 to 49,000 across the EU.[2] The CSRD officially entered into force in January 2023 and is effective from 1st January 2024 for large companies with more than 500 employees. Other companies will be required to report in the following years. Although the directive has not yet been transposed into German law, the member states of the EU have 18 months to transpose it into national law after the CSRD has entered into force. The CSRD, on the one hand, is refering to the EU Taxonomy by requesting the reporting requirements under Article 8 of the EU Taxonomy.[3] On the other hand, the CSRD refers to the ‘Greenhouse Gas Protocol’ (GHG) and its concept of scopes. In this regard, Article 47 of the CSRD requires that information relating to Scope 3 emissions must be included in the sustainability reporting. This article also makes clear that although the CSRD describes the disclosure requirements, no requirements are made with regard to which kind of information are to be disclosed. With reference to Article 29b of the CSRD, the European Commission must therefore establish further standards for sustainability reporting. [4] On the 22nd November 2022, the first draft of the ‘European Sustainability Reporting Standards’ (ESRS) was therefore published by EFRAG as a technical consultant to the Commission.[5] In particular, ESRS should take into account and reflect international regulations. The relationship between the ESRS and the EU Taxonomy, as well as the SFDR and other regulations, are described in the Explanatory Note [6]. Equally to the CSRD, the ESRS must also be implemented by January 2024. First reports under CSRD are to be published as of 2025.[7]

The ESRS are sector-agnostic and consist of 12 so-called ‘Exposure Drafts’ (ED), which in turn are divided into two cross-sector EDs (ESRS1 + ESRS2), as well as ten topic-specific EDs. In total, ESRS include 82 ‘Disclosure Requirements’ (DR), divided into the twelve different EDs.

Figure 1: Overview of DRs per ED [8]

All companies falling within the scope of ESRS must comply with and implement the requirements of the two sector-agnostic EDs ESRS 1 and ESRS 2. [9] In order to analyse which requirements of the topic-specific EDs from the ESRS E1-5, S1-4 and G1 are to be implemented, companies must carry out a “materiality analysis”. The materiality analysis shall be carried out for all topic-specific ESRS. Once an issue has been defined as material in accordance with ESRS 1, Section 3.4 and 3.5, it must be disclosed in accordance with the disclosure requirements of the respective standard.[10] The result of this analysis determines which disclosure requirements are to be presented in a report.

As required by the CSRD, ESRS follows the principle of ‘double materiality’. This means that companies, regardless of industry, need to do sustainability reporting from two perspectives:

- Impact materiality: How does the company affect people and the environment? Actual or potential, positive, and negative impacts of the company on people and the environment must be considered. This includes impacts that are directly caused by activities, products, and services of the company, as well as impacts that result from business relationships of the value chain (upstream & downstream).[11]

- Financial Materiality: How do the environment and people influence the company? The impact of environmental and social factors on the company’s cash flow, cost of capital, and access to finance must be considered. This includes information about risks and opportunities related to business relationships. [12]

Although all disclosure requirements are to be integrated into the annual report in accordance with the respective materiality analysis in the future, ESRS offers a transitional period to implement the requirements. Annex D of ESRS 1 lists the requirements (DRs) that may first be omitted or that must be implemented at a later point in time. [13]

In the previous section, the current requirements of CSRD and ESRS have now been outlined. No distinction has been made for different industries up to now. But what does this mean for financial institutions that differ significantly from other industries in their business models?

As mentioned above, the CSRD, and therefore the ESRS, refers to the concept of the ‘Greenhouse Gas Protocol’ (GHG), whereby emissions must also be disclosed in Scope 1, 2, and 3. In particular, Scope 3 emissions are of central importance for banks and insurers because most of the emissions caused are not from their own sources, but from financial instruments or insurance activities. This corresponds to the definition of Scope 3 emissions, which include all indirect emissions from sources that are not owned or controlled by the company. Scope 3 Emissions correspond to emissions that occur in the company's value chain.[14] It is estimated that Scope 3 emissions for banks and insurers are 700 times larger than direct Scope 1 and Scope 2 emissions.[15]

The EFRAG Draft ‘Implementation Guidance for Value Chain’ (VCIG) explains the extent to which emissions from the value chain are to be included in the materiality analysis and, consequently, in the calculation and disclosure. For banks and insurers, this means that emissions from investments made, as well as emissions from loans or insurance issued, would have to be calculated and disclosed. However, to implement this, information is required from the borrowers and policyholders, some of which are not publicly available.

For the financial industry, the question here is how to include information from business partners and customers in the calculation and disclosure of sustainability metrics.

In the VCIG, EFRAG does not provide a clear answer to the ‘HOW’. It is noted that “financial assets”, including loans and investments, are interpreted as “business relationships” and therefore fall within the scope of the value chain.[16] For example, if the company grants loans to another company, which is ultimately used to implement a project that in turn leads to water pollution, this influence must also be attributed to the lender.[17]Although it is established that the indirect Scope 3 emissions of financial institutions must also be calculated and disclosed, no standards have been published so far to implement these requirements for financial institutions by EFRAG or other European institutions.[18]

For this reason, the draft ESRS has so far referred to other initiatives. ESRS requires financial institutions to use the requirements of the ‘Greenhouse Gas Accounting and Reporting Standard for Financial Industry’ (PCAF) to disclose Scope 3 emissions.[19] The ‘Partnership for Carbon Accounting Financials (PCAF)’, which develops this standard, is a global partnership of different financial institutions that jointly develops approaches to assess and disclose greenhouse gas emissions related to loans and investments.[20] In principle, accession to the partnership is voluntary, but application of the PCAF standards is mandatory upon accession. [21]

Based on the ‘GHG Corporate Accounting and Reporting Standard’ and the ‘Corporate Value Chain (Scope 3) Accounting and Reporting Standard’, the PCAF Standard provides standardized methods for measuring “financed” and “insured emissions”. This will continue to enable financial institutions to develop new strategies and innovative financial products. The PCAF standards consist of the following three parts:

Part A ‘Financed Emissions’ includes the calculation methods for measuring and disclosing emissions related to different asset classes.

Part B ‘Facilitated Emissions’ provides calculation methods to determine the issues related to capital market transactions.

Part C ‘Insurance Associated Emissions’ includes calculation methods for determining issues related to insurance and reinsurance. [22]

However, for the calculation of Scope 3 emissions, ESRS refers only to ‘financial institutions’. There is no definition of the term ‘financial institution’, including a clear distinction between banks and insurance companies. In addition, ESRS requires screening of Scope 3 emissions based on the 15 Scope 3 categories of the ‘GHG Protocol Corporate Standard’ and the ‘GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard’.[23] However, these 15 Scope 3 categories do not cover insurance business. Therefore, the ESRS is assumed to refer only to Part A of the PCAF standard (‘Financed Emissions’) and emissions related to insurance (‘Insurance Associated Emissions’=IAE) are not taken into account. It is therefore important to clarify how the IAE are to be calculated and disclosed. Associations, including the Association of the German Insurance Industry, demand sector-specific ESRS for insurance, as well as more lead time for implementation.[24] For the given reason, the focus of the following section is therefore only on 'Financed Emissions'.

The application of the PCAF standards primarily serves to measure and disclose the greenhouse gas emissions caused by investments and credits. The measurement of these emissions forms the basis for identifying risks and opportunities associated with the formation of greenhouse gases and thus enabling decarbonization. In addition, the results of these calculations serve as a basis for the development of strategies and products to enable the achievement of climate targets.

Figure 2: PCAF as a start to achieve climate objectives [25]

The PCAF standard for ‘Financed Emissions’ (Part A) includes calculation methods for seven different asset classes, whereby separate requirements are described for each class:

- Listed equity and corporate bonds

- Business loans and unlisted equity

- Project Finance

- Commercial real estate

- Mortgages

- Loans for motor vehicles

- Sovereign Debt

A method is also provided by PCAF to determine which asset category is to be applied for each financial product. The determination takes place in three steps and follows the ‘follow-the-money principle’:

- Definition of Type and Source of Financing

- Corporate Finance: Financing Companies

- Project Finance: Financing Projects

- Consumer Finance: Financing for Private Customers

- Determination of the “Use of Proceeds”, as well as the industry or financing activity

- Determination of what the financial resources are used for.

- Assignment of asset class as described above. [26]

Figure 3: Derivation of the applicable asset class and calculation method [27]

Once the asset class is determined, the emissions can be calculated. The PCAF standard thereby follows the attribution principle. According to the ‘GHG Protocol Value Chain Accounting and Reporting Standard’, GHG issues from loans and investments are to be allocated to the financial institution based on the share of loans and investments in the borrower. In other words, the financial institution is responsible for a share of the emissions of the borrower.

The calculation of the ‘Financed Emissions’ is done for all asset classes equally, based on the annual emissions of the borrower. To do this, an attribution factor is first calculated. This is the share of the remaining amount of a loan or investment (numerator) in the total equity and debt of the company or project to which the financial institution provides capital (denominator). This “attribution factor” must afterwards be multiplied by the total emissions of the borrower. A differentiation of the applicable value in the denominator results from the methods to be used for the asset classes.[28]

Figure 4 : PCAF calculation formula

The calculation of the ‘Financed Emissions’ requires, as described, information about the emissions of the borrower. This information is either provided by the borrower or can often already be taken from a sustainability report from the borrower. However, the quality of this data can vary between companies with regard to e.g. timeliness and correctness. For this reason, PCAF also provides a scoring model to evaluate the quality of the underlying data.

Figure 5: PCAF Data Quality Scoring Model

The scoring model consists of five levels, where data classified with 'Score 1' potentially has the best data quality. ‘Score 5’ represents the potentially worst data quality. Data quality scoring is different for each asset class. Basically, it is advised to use the best possible data but PCAF dictates what kind of information to use in each score for each asset class.[29] These are listed and explained in the appendix to the ‘Financed Emissions’ standard for each asset class. The following image shows the options using project financing as an example. Here you can clearly see the differences in the information to be applied and their accuracy in the individual scores.

Figure 6: Data Quality Score for Project Financing[30]

In summary, PCAF is a good approach to calculating financed and insured emissions. Nevertheless, the standard does not allow a complete and accurate presentation of Scope 3 emissions from financial institutions. Firstly, there seem to be no clear recommendations by ESRS for insurance companies, which means it is up to the companies themselves to determine which calculation method is to be used for Scope 3 emissions. As a result, comparability between insurers in terms of their Scope 3 emissions would be hampered. On the other hand, as described, PCAF also allows the use of different data qualities. While PCAF also provides a scoring model to standardize data qualities, this means that financial institutions may also use incomplete or even unverified information about customers to calculate emissions from financing and investment activities. Although the data quality score must be disclosed in addition to the metric, heterogeneous data quality leads to a difficult internal comparability between parts of the portfolio, as well as externally between companies and projects.

The fact is that financial institutions have to implement the requirements of the CSRD, and therefore the requirements of ESRS, partially as of January 2024. Even though it appears no clear requirements for the calculation and disclosure of Scope 3 emissions have been published for insurance companies, financial institutions are already asked to use the PCAF standard to calculate the Scope 3 emissions from financing and investment activities. However, these are one of the biggest challenges financial institutions are facing. In particular, the availability and validation of customers’ sustainability information is a challenge. In addition, financial institutions need to find technical solutions to store the collected information of business partners and customers in a consolidated manner and, based on this, to calculate and disclose the key figures required by the regulatory frameworks.

SAP’s sustainability portfolio can help financial institutions to overcome these challenges. In a following blog post, the current SAP portfolio for sustainability in the financial industry shall be presented and explained. In particular, the technical implementation of the regulatory requirements of the CSRD and ESRS is planned to be examined in more detail.

References:

[1] EU Taxonomy Regulation (EU) 2020/852

[2] CSR - Corporate Sustainability Reporting Directive (CSRD)

[3] CSRD - DIRECTIVE (EU) 2022/2464 - (46)

[4] CSRD - DIRECTIVE (EU) 2022/2464 – Article 29(b)

[5] EFRAG, November 2022 - ESRS Cover Letter

[6] EFRAG, November 2022 – ESRS Explanatory Note

[7] EFRAG - First Set of Draft ESRS

[8] Cf. ESRS, Appendix I Disclosure Requirement Index – Table 2 ‘Overview of DRAFT ESRS’

[9] ESRS 1 – November 2022, Chapter 3.2

[11] ESRS 1, November 2022, Chapter 3.4

[12] ESRS 1, November 2022, Chapter 3.5

[13] ESRS 1, November 2022, Chapter 10.4 & ESRS 1 – November 2022, Appendix D

[14] Corporate Value Chain (Scope 3) Accounting and Reporting Standard, Chapter 5

[15] S&P Global – Podcast ‘How financial institutions are tackling Scope 3 funded emissions’

[16] EFRAG – Implementation Guidance for Value Chain (VCIG), 23. August 2023, para. 56

[17] ESRS 1 – November 2022, AR 7(b)

[18] EFRAG – Implementation Guidance for Value Chain (VCIG), 23. August 2023, para. 58

[19] ESRS E1, November 2022, Appendix B, AR 44 (b)

[20] PCAF – About PCAF

[21] PCAF - How to Join PCAF

[22] PCAF - The Global GHG Accounting and Reporting Standard for the Financial Industry

[23] ESRS E1, November 2022, Appendix B, AR 44 (c)

[24] GIA – Comment on the first set of draft European Sustainability Reporting Standards

[25] PCAF – Financed Emissions Standard

[26] PCAF - ‘Financed Emissions’ Standard – Chapter 5

[27] PCAF - ‘Financed Emissions’ Standard – Chapter 5, Figure 5-1.

[28] PCAF - ‘Financed Emissions’ Standard – Chapter 4 & Chapter 5

[29] PCAF - ‘Financed Emissions’ Standard – Chapter 4.2

[30] PCAF - ‘Financed Emissions’ Standard, Annex 10.1, Table 10.1-3

- SAP Managed Tags:

- Banking,

- Insurance,

- Sustainability

You must be a registered user to add a comment. If you've already registered, sign in. Otherwise, register and sign in.

Labels in this area

-

Banking

1 -

BTP for Sustainability

2 -

Circular Design

1 -

Circular Economy

1 -

Compliance

1 -

CSRD

1 -

EPR

1 -

ESG

1 -

ESRS

1 -

Financial Services

1 -

Insurance

1 -

Packaging

1 -

PCAF

1 -

Picking Strategy

1 -

Plastic Taxes

1 -

Recyclability

1 -

SAP Analytics Cloud

1 -

SAP Cloud for Sustainable Enterprises

1 -

SAP Community

1 -

SAP Datasphere

1 -

SAP Profitability and Performance Management

1 -

SAP Responsible Design and Production

1 -

SAP SCT

1 -

SAP Sustainability Control Tower

2 -

SAP Sustainability Footprint Management

1 -

SCT

1 -

Sustainability

1 -

Sustainability Control Tower

1 -

Sustainable Finance

1